Ep. 205 – April Market update: Budget night and rising rents … how do we solve this issue?

Ep. 205 – April Market update: Budget night and rising rents … how do we solve this issue?

Mike opens his first official Market Update episode and kicks off the conversation with the Federal Government’s budget night announcements. Notably, the trio talk about the impact on the property market, in particular the measures that are proposed to ease the cost of living and the government’s approach to tackle the rental crisis.

The Trio ponder the complexities of long lead time and expensive building costs when it comes to targeting the new supply side of the equation, and Cate points out the contrasts between this particular budget night and past budget nights.

Dave discusses the Build to Rent sector and the challenges that this initiative poses for the government, and he sheds light on the management trust withholding tax changes and the impact that this proposed easing will have on investment in the sector. Cate’s word of caution about this type of investment category with controlled rents is an interesting one for pragmatic investors to consider.

The initiative that the Trio all agree is a good one is the First Home Buyer shared equity scheme. Opening up the offering to those who have previously owned a home more than ten years prior, and allowing siblings and friends to co-purchase is a significant change to what was already a good offering.

“It’s much harder these days to buy a property as a single”, says Dave, and this opportunity will make a positive difference for a lot of Australians, (including permanent residents) who are keen to get a foot on the property ladder.

Cate particularly likes this initiative for several reasons, including the fact that it is less likely to segment the market and result in a dual speed rate of growth for first homebuyer stock vs all other stock.

The side impacts that could increase house prices in specific areas include parental leave changes, (as household incomes grow), and green energy infrastructure upgrades in our existing steel manufacturing locations.

Moving into our April Market Update…

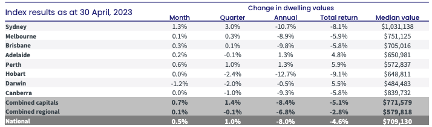

As Dave points out, Sydney is the “absolute standout”, but other capital cities are also rebounding. Low listings, record new arrivals and a general stabilisation of rate increases are the current tailwinds behind the property market.

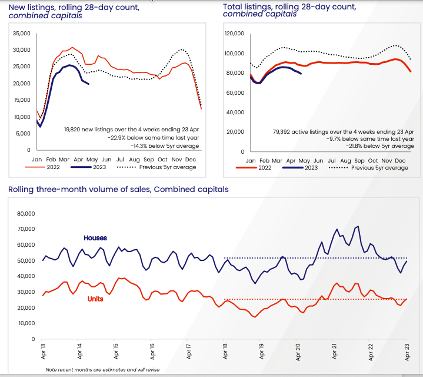

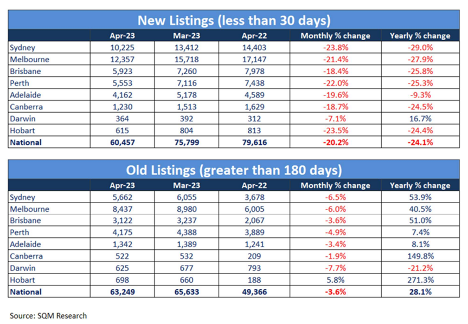

Cate speaks about listing volumes and the drivers that influence them. Currently, vendor participation is low, and buyers are pouncing onto ‘old stock’, which is in turn eroding ‘all stock’. Negative media sentiment and data lag are likely drivers of the current low listing rates.

“Until vendors have confidence that the market isn’t horrible, vendors are going to sit on their hands”, says Cate. And she also shares her concerns about a particularly quiet winter; something that will be difficult for buyers, especially in the cooler climate cities.

Dave also comments about something important: listing activity is also low because owner tenure is extended. People are holding their properties for longer.

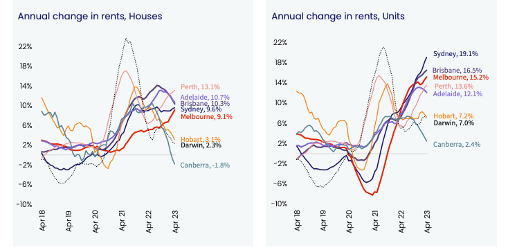

The annual change in rents for houses continues to challenge several markets, but the change in unit rents is quite shocking for tenants in the affected cities and regions. But why is Tasmania lagging when compared to the other states? Mike asks Cate to explain and her answer may surprise listeners. And what is the story with Canberra? Dave eludes to the challenges associated with the public sector wage freezes, combined with the work from home acceptance.

Cate’s curious finding about eastern seaboard capital city top rental performers is intriguing…. we won’t spoil the surprise.

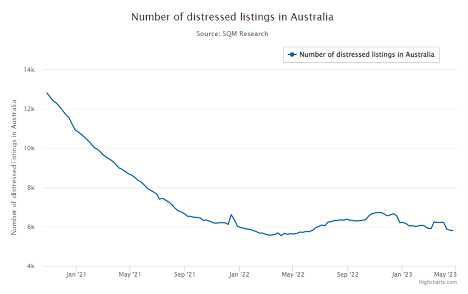

Distressed listings are not as ‘distressed’ as the media would have had us believe. The charts are not showing that the impact of interest rate increases have dismantled home ownership like the headlines suggested they would.

The trio focus their attention on the Westpac Consumer Sentiment Index and debate some of the drivers and changes that are noteworthy forward indicators for our housing market.

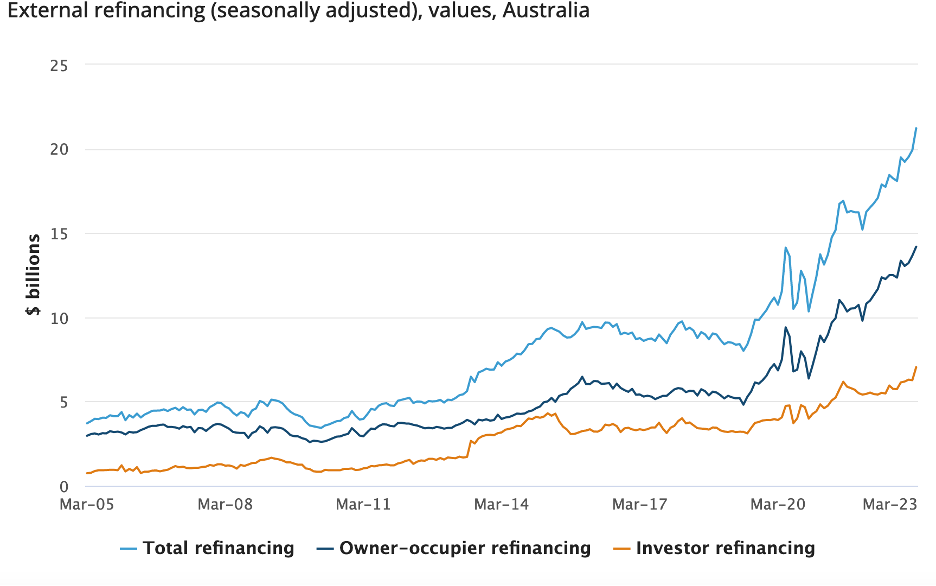

New loan commitments are interesting, and according to Mike, “the refinancing goldrush has become a hallmark of 2023”. Dave discusses a rebound he’s seeing; both owner-occupier financing group and the investor financing groups have grown in size. First home buyers have grown by 15%; possibly amplified by the NSW stamp duty changes.

And… time for our gold nuggets…

Dave Johnston’s gold nugget: the separation between unit rental growth and house rental growth is a great one to watch. We saw cyclical highs in the last quarter, and Dave is tracking the relative historical differential between unit and house rents with an educated hunch that we could see units turn a corner.

Cate Bakos’s gold nugget: Any prospective vendors who are wondering if/when it will be a good time to sell. Cate implores them to hit the pavement and to check out some auctions in their area. They may be pleasantly surprised.

Mike Mortlock’s gold nugget: Mike points out that we’ve seen the data starting to turn around, and he says it’s important to understand data lag. The best way to get a feel for the up-to-the-minute market conditions is to jump into the coal face and experience it in person.

If you’ve enjoyed this episode you may like to listen to these eps:

Ep. 10 – Why your approach and assessment of risk is paramount to property success

Ep. 12 – Property cycle management

Ep. 19 – Time IN the market vs TIMING the market

Ep. 31 – Get rich quick schemes

Ep. 158 – how interest rate cycles have impacted the property market since 1990